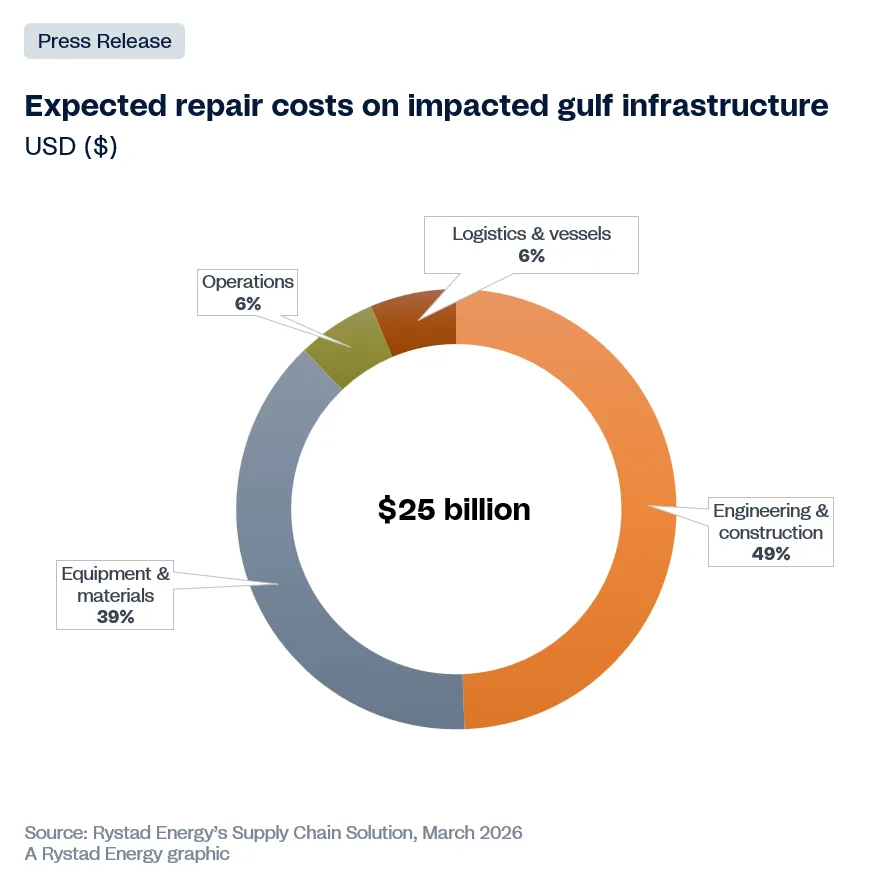

The armed conflict in the Middle East has left an energy infrastructure bill that Rystad Energy estimates at at least $25 billion in repair and infrastructure restoration costs. The analysis, published on April 15, assesses the condition of liquefied natural gas (LNG) plants, refineries, fuel terminals, and gas-to-liquids conversion facilities across the region.

The breakdown of projected spending places engineering and construction as the dominant item, followed by equipment and materials. However, Rystad underscores that the initial figure will increase as damage assessments are completed at facilities that still remain inaccessible for a full technical audit.

Beyond the financial magnitude, the report warns that capital alone will not guarantee the recovery of energy infrastructure. Restoration timelines will vary drastically depending on the type of damaged asset, the availability of critical equipment in international markets, and local capacity to execute EPC (engineering, procurement, and construction) projects.

Process bottleneck: LNG turbines with no manufacturers

The most revealing finding in Rystad’s analysis—and the one with the greatest structural impact on natural gas markets—is not the total damage, but the identification of logistical constraints in the manufacturing phase that existed before the conflict and that the war has made critical: the large-scale gas turbines for main refrigeration compressors at LNG plants.

These units are supplied globally by only three original equipment manufacturers (OEMs). As 2026 began, all of them were already facing production delays of between two and four years, a direct consequence of rising demand driven by data center electrification and the accelerated shutdown of coal-fired power plants in Europe and Asia.

The implication is straightforward: a severely damaged LNG plant in Ras Laffan will not be able to restart operations based on when repair capital arrives for the energy infrastructure, but on when it can secure a place in the turbine delivery queue—an outlook that today exceeds four years for new orders.

Ras Laffan and South Pars: energy infrastructure

Ras Laffan Industrial City in Qatar represents the most severe case in the analysis. The destruction of the S4 and S6 LNG plants has triggered a force majeure declaration and a 17% capacity reduction, equivalent to 12.8 million tonnes per annum (Mtpa). Rystad estimates that full recovery could take up to five years, precisely due to dependence on the aforementioned refrigeration turbines.

Iran’s offshore South Pars field presents additional geopolitical complexity. Western sanctions exclude Iran from access to European and North American contractors and technology, forcing Tehran to rely on Chinese and domestic contractors. While technically viable, this route may be slower and more costly, and urgent repairs will need to be prioritized over any previously announced expansion plans.

The local EPC advantage: Saudi Aramco as a benchmark

In contrast to the most urgent cases, Rystad’s analysis identifies an illustrative counterpoint: Saudi Aramco’s operations in Ras Tanura, where maintenance teams were already on site carrying out a scheduled shutdown when debris fell within the facility perimeter. The proximity and density of the national EPC ecosystem enabled an immediate response that accelerated the restart of operations.

This episode highlights the variable that, according to Rystad, most influences recovery trajectories and is often underestimated in conventional damage assessments: the installed EPC execution capacity in the vicinity of each asset.

Source and Photo: https://www.rystadenergy.com/